")

Most people quote LTV when they talk about “risk.”

But when you buy notes at a discount, LTV can describe the loan and still miss your exposure.

At 7e, we track LTV, but we underwrite decisions around Investment-to-Value (ITV) because it ties risk to the only number you actually control: your cost basis.

Why LTV Doesn’t Tell You What You Paid

The problem with LTV is that it’s based on what the borrower owes and not what we actually pay to acquire the loan.

In many cases, we buy notes at a discount. A borrower might owe $200,000, but if we acquire the note for $100,000, our real exposure isn’t reflected in the LTV.

That brings us to a more accurate metric: Investment-to-Value (ITV).

What Is Investment-to-Value (ITV)?

ITV = Purchase price ÷ Current property value

In the example above, $100,000 ÷ $200,000 = 50% ITV.

That’s the number that matters to us. It tells us:

- Our true exposure

- How much cushion we have if property values decline

- How flexible we can be in restructuring, repayment plans, or liquidation

LTV Is the Lender’s View. ITV Is the Investor’s Reality

LTV answers the question: How much of the property’s value is covered by the loan balance?

ITV answers a more relevant question: What did we actually pay, and how protected is our capital?

Example:

- Property value (as-is): $1,000,000

- Senior loan: $650,000

- CapEx + reserves: $250,000

- Total capital invested: $900,000

LTV: 65%

ITV: 90%

Now imagine that value drops to $900,000. LTV is still within tolerance. But ITV is now 100%, meaning all capital is at risk.

Why ITV Matters More in Today’s Market

In 2026, with interest rates in flux, borrower uncertainty rising, and regional market softness in play, we underwrite for one thing: margin.

We bid based on ITV, not just LTV, because:

- It reflects our real cost basis

- It gives us room for outcomes that aren’t perfect

- It supports flexibility in recoveries, modifications, and exits

We pass on notes that have “safe” LTVs but price tags that leave no room for risk. We target discounted acquisitions with capital structures that support both resolution and investor distributions.

Why Discounted Note Purchases Make LTV Misleading

LTV often reflects original underwriting, not current economics.

Scenario:

- Property value: $250,000

- Original loan balance: $300,000 (120% LTV)

- Investor purchase price: $100,000

Investor ITV: 40%

This shows why we ignore face value and focus on cost basis. ITV tells us if we can afford to be patient, strategic, or creative.

What 7e Pressure-Tests in Every Tape

1. What type of value is being used?

As-is value creates more conservative ITV math than ARV.

2. Are all capital layers counted?

We include rehab, reserves, equity, capitalized fees, and carry.

3. What happens if exits are delayed or financing tightens?

ITV shows how much cushion exists if market or timing shifts.

4. In a workout, who funds and how much?

Our ITV discipline helps avoid underestimating stabilization costs.

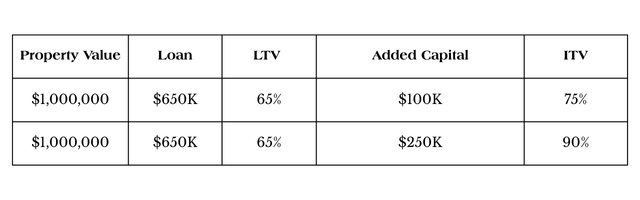

Same Deal, Different ITV — And Different Risk

Both have the same LTV. But the second deal has far less room for error. That difference matters more in 2026 than ever before.

Bottom Line: We Don’t Chase LTV. We Bid on ITV.

At 7e, we’re not just underwriting borrowers, we’re underwriting the price we pay to take on the risk.

Because for us and our investors, it’s not about what’s owed. It’s about:

- What we paid

- What we control

- How we manage the path forward

Questions to Ask Before Submitting a Tape or Allocating Capital

- What is the ITV, not just the LTV?

- Does ITV include reserves, capex, and fees?

- What kind of value is being used (as-is vs ARV)?

- How much price decline can the deal absorb before impairing capital?

- Who funds the workout and where do they sit in the stack?

Disclaimer: This article reflects market commentary and operational perspective drawn from a referenced transcript and is for educational purposes only. It is not investment, legal, or tax advice. Past performance is not a guarantee of future success.

Continue Exploring Note Investing With 7e

Ready to Start Investing?